A statutory demand is one of the most powerful debt recovery tools available to creditors in Australia. Issued under section 459E of the Corporations Act 2001 (Cth), it gives a company debtor 21 days to pay — or face a presumption of insolvency and the threat of being wound up. This guide explains when to use a statutory demand, how to serve one correctly, the 21-day timeline, and the common pitfalls that can undermine the process.

What is a statutory demand?

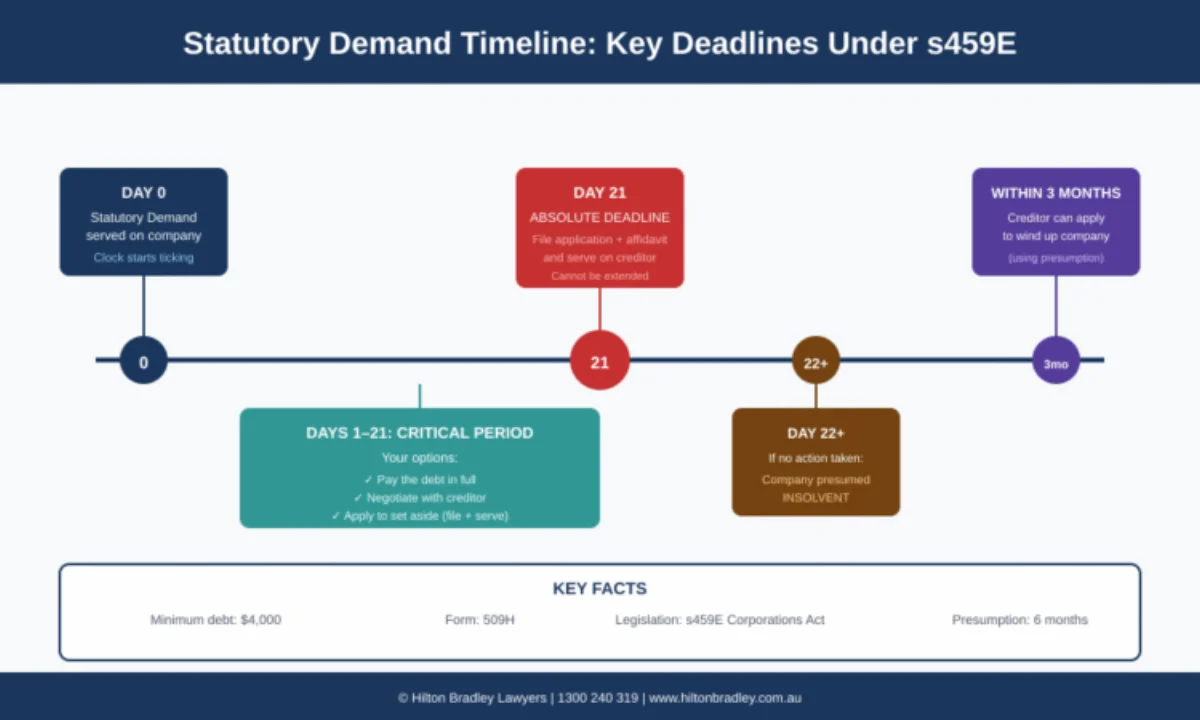

A statutory demand is a formal written notice served on a company, requiring it to pay a debt that is due and payable and totals at least $4,000. It is not a court process — you don't need to file anything with the court to issue one. But it triggers serious legal consequences if the company fails to comply.

If the company doesn't pay, secure the debt, or apply to have the demand set aside within 21 days, a presumption of insolvency arises under section 459C(2) of the Corporations Act. The creditor can then apply to the court to wind the company up. That threat is what makes statutory demands so effective — most directors would rather pay the debt than risk their company being wound up.

When to use a statutory demand

A statutory demand works best when:

- The debt is due and payable — not contingent, prospective, or subject to conditions

- The debt is not genuinely disputed — if the debtor has a legitimate argument that the debt isn't owed, the demand will be set aside

- The debt is $4,000 or more — the statutory minimum threshold

- The debtor is a company (Pty Ltd, Ltd) — statutory demands can't be used against individuals or sole traders

- The debtor is avoiding payment rather than genuinely unable to pay — though the demand works in both cases

A statutory demand is not appropriate when the debt is genuinely disputed, the debtor is an individual, you're owed less than $4,000, or you want a money judgment (use court proceedings instead).

How to serve a statutory demand

The demand must be in the prescribed form (Form 509H under the Corporations Regulations 2001) and must be accompanied by an affidavit that verifies the debt is due and payable. Getting the form and affidavit right is critical — defects can give the debtor grounds to have the demand set aside.

Service must be at the company's registered office as recorded with ASIC. You can find this on the ASIC company register. Methods of service include:

- Leaving the demand at the registered office

- Posting it by prepaid post to the registered office

- Personal service on a director of the company

Do not serve the demand at a trading address that isn't the registered office — defective service can give the debtor an argument for setting the demand aside, even if they actually received it.

The 21-day period

Once the demand is served, the clock starts. The company has exactly 21 days to:

- Pay the debt in full

- Secure or compound the debt to the creditor's reasonable satisfaction (e.g., provide a bank guarantee or enter into a binding payment arrangement)

- Apply to the court to have the demand set aside under section 459G

The 21-day period is strict. It cannot be extended by the court or by agreement between the parties. If the company misses the deadline — even by one day — it loses the right to apply to set aside the demand, and the presumption of insolvency kicks in.

Grounds to set aside a statutory demand

| Ground | What it means |

|---|---|

| Genuine dispute (s459H(1)(a)) | There's a real, not spurious, dispute about whether the debt exists or its amount. The threshold is low — you need only show a "plausible contention requiring investigation." |

| Offsetting claim (s459H(1)(b)) | The company has a genuine counterclaim against the creditor that reduces or exceeds the debt claimed. If the offsetting claim brings the net amount below $4,000, the demand must be set aside. |

| Defect in the demand (s459J(1)(a)) | The demand has a defect (wrong amount, wrong company name, missing information) that would cause substantial injustice if not set aside. |

Common pitfalls

Statutory demands are straightforward in theory but easy to get wrong in practice. Here are the mistakes we see most often:

- Using it for a disputed debt. If there's a genuine dispute about whether the debt exists or its amount, the demand will be set aside. Use normal debt recovery proceedings instead.

- Wrong company name or ACN. The demand must correctly identify the debtor company as registered with ASIC. Misspellings or using trading names instead of legal names can be fatal.

- Overstating the amount. Including amounts that aren't yet due, or inflating the debt with disputed charges, opens the door to a genuine dispute argument.

- Defective affidavit. The supporting affidavit must comply with court rules and shouldn't pre-date the demand. A defective affidavit can sink the whole process.

- Serving at the wrong address. The demand must be served at the registered office, not a trading address or branch office. Always check the ASIC register before serving.

- Delay after the 21-day period expires. Once the 21 days pass, don't wait months to file a winding-up application. Courts have discretion to dismiss applications where the creditor has delayed unreasonably.

What happens after the 21 days?

If the company doesn't comply with the demand and doesn't apply to set it aside within 21 days, you can apply to the court for an order that the company be wound up in insolvency. The presumption of insolvency means the company bears the onus of proving it is solvent — a reversal of the usual burden of proof that gives you a significant tactical advantage.

In practice, the winding-up application itself often prompts payment. Most companies — even those that have been stalling for months — find the money when faced with the prospect of a liquidator being appointed.

Key takeaways

- A statutory demand is a formal notice under s459E requiring a company to pay a debt of $4,000+ within 21 days

- Non-compliance creates a presumption of insolvency — the creditor can then apply to wind the company up

- The 21-day deadline is absolute and cannot be extended

- Don't use a statutory demand for genuinely disputed debts — it will be set aside with costs

- Get the form, affidavit, company name, and service address right — defects can be fatal

- A specialist debt recovery lawyer should prepare and serve the demand to avoid costly errors

Need to issue a statutory demand or respond to one? Call Hilton Bradley on 1300 240 319 for a free consultation.

Disclaimer: This article provides general information about statutory demands under Australian law as at February 2026. It is not a substitute for legal advice specific to your situation. For advice tailored to your circumstances, contact Hilton Bradley on 1300 240 319.

Disclaimer: The information in this article is general in nature and should not be relied upon as legal advice. Please seek professional advice tailored to your particular circumstances.

Kieran Kelly

Director

Kieran is a Director at Hilton Bradley with litigation experience since 2012, focusing on banking and insolvency disputes.

View profile →