Late payments don't happen by accident — they happen when businesses don't have a clear system for managing credit and chasing overdue accounts. A written credit control policy gives your team a step-by-step process for extending credit, invoicing promptly, and escalating when payments fall overdue. This guide includes a policy template you can adapt for your business and a 90-day recovery flow that takes you from first reminder to legal action.

What a credit control policy should cover

| Policy Element | What to Include |

|---|---|

| Payment terms | Standard terms (e.g., 14 or 30 days from invoice). Specify when payment is due, accepted methods, and any early payment discounts. |

| Credit assessment | How you evaluate new customers before extending credit. Include credit checks, trade references, and credit limits by risk category. |

| Credit limits | Maximum credit by customer tier. Set thresholds that trigger review (e.g., any single order over $20,000 requires credit manager approval). |

| Invoicing standards | Invoice within 24 hours of supply. Include ABN, payment terms, bank details, and reference number on every invoice. |

| Overdue process | Step-by-step escalation timeline (see the 90-day flow below). Define who is responsible at each stage. |

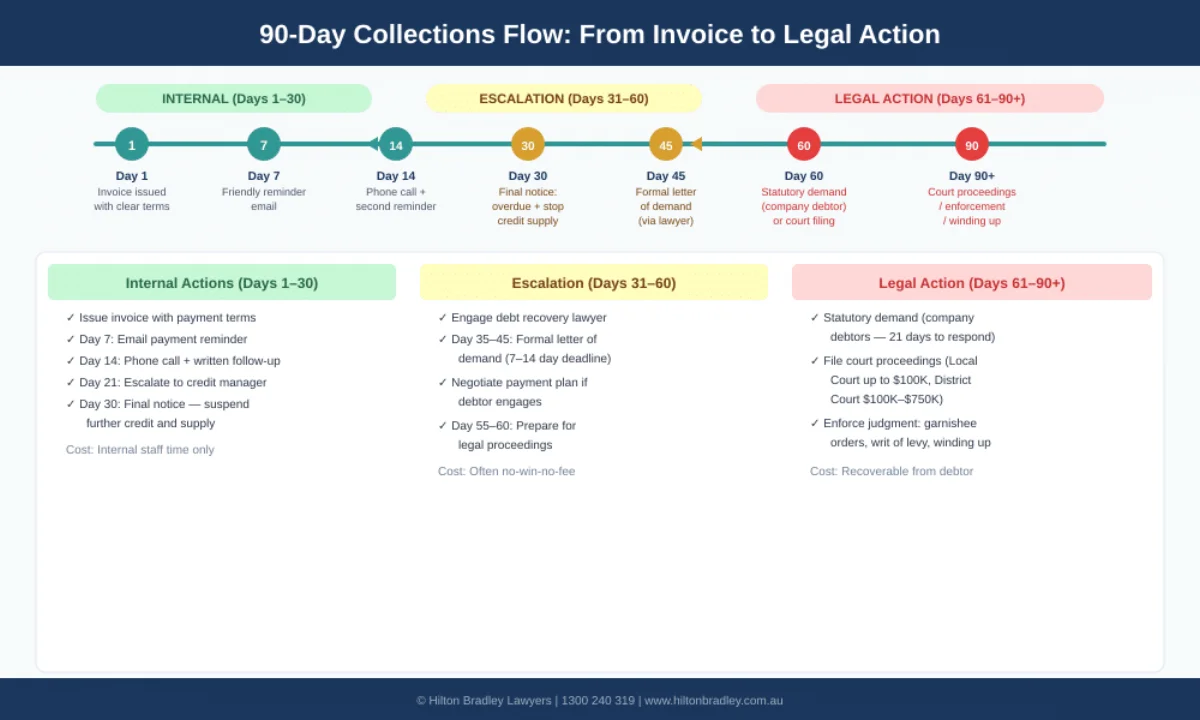

The 90-day overdue recovery flow

Days 1–30: Internal follow-up

This is where most overdue invoices should be resolved. The key is acting early and consistently — don't wait until day 30 to make your first contact.

- Day 1 (invoice due date): Send a payment reminder by email. A simple, professional reminder is often all it takes — many late payments are simply oversights.

- Day 7: Follow up with a phone call to the accounts payable contact. Confirm they received the invoice, ask when payment will be processed, and note the commitment in your records.

- Day 14: Send a second written reminder, this time with firmer language. Reference the original invoice, the payment terms, and the commitment made during your phone call.

- Day 21: Escalate internally. If the account contact isn't responding, go to a more senior person in the debtor's business. A polite but direct email to the business owner or financial controller often produces results.

- Day 30: Issue a final internal reminder. State clearly that if payment is not received within 7 days, the matter will be referred to your solicitors for formal recovery. This is your last opportunity to resolve the matter before incurring legal costs.

Days 31–60: Formal demand

If internal follow-up hasn't worked, it's time to escalate. At this point, the debtor has had the invoice for at least 60 days and has been reminded multiple times. The debt is no longer an oversight — it's a decision not to pay.

- Day 31–35: Refer the matter to your debt recovery lawyer. Provide copies of the contract, invoice(s), delivery records, and all correspondence.

- Day 35–40: Your lawyer issues a formal letter of demand. This letter should specify the exact amount owed, the legal basis for the debt, a deadline for payment (typically 7–14 days), and the consequences of non-payment — including court proceedings or statutory demand.

- Day 40–60: Allow the deadline to pass. Many debtors pay during this window. If the debtor responds with a genuine dispute, work with your lawyer to assess whether the dispute has merit and adjust your strategy accordingly. If the debtor ignores the demand or makes excuses, prepare to escalate.

Days 61–90+: Legal action

- For company debtors: Your lawyer can issue a statutory demand under s 459E of the Corporations Act 2001 (Cth). The company has 21 days to pay or face a presumption of insolvency — and the threat of being wound up.

- For individual debtors: File a statement of claim in the appropriate court (NSW Local Court for debts up to $100,000).

- Enforcement: Once you have a judgment, enforcement options include garnishee orders, writs for levy of property, and examination notices.

- Cost recovery: In most cases, the court can order the debtor to pay your legal costs — so the cost of engaging a lawyer doesn't come out of your recovery.

Three things most credit control policies get wrong

Even businesses with a written policy often make the same mistakes. Here's what to watch for:

- No one owns the process. A policy that sits in a drawer is worthless. Assign a specific person (or team) responsibility for each stage of the recovery flow. If no one is accountable, nothing happens.

- Escalation is too slow. Many businesses wait 90 or even 120 days before involving a lawyer. By then, the debtor may have disappeared, dissipated assets, or become insolvent. The 90-day flow above is designed to have legal action underway within 60 days of the due date — fast enough to maximise your chances of recovery.

- No credit assessment upfront. Extending credit without assessing the customer's ability to pay is asking for trouble. A basic credit check and trade references cost very little compared to the cost of chasing a bad debt for months.

Key takeaways

- A written credit control policy with clear ownership and timelines is the foundation of healthy cash flow

- Invoice within 24 hours, follow up on day 1 of overdue, and escalate to a lawyer by day 31

- The 90-day flow moves from internal reminders (days 1–30) to formal demand (days 31–60) to legal action (days 61–90+)

- For company debtors, a statutory demand is one of the fastest and most cost-effective escalation tools

- Don't wait 90+ days to involve a lawyer — the sooner you escalate, the better your chances of recovery

- Run credit checks on every new customer before extending trade credit

Need help setting up your credit control process or recovering overdue accounts? Call Hilton Bradley on 1300 240 319 for a free consultation.

Disclaimer: This article provides general information about credit control and debt recovery under Australian law as at February 2026. It is not a substitute for legal or financial advice specific to your business. For advice tailored to your circumstances, contact Hilton Bradley on 1300 240 319.

Disclaimer: The information in this article is general in nature and should not be relied upon as legal advice. Please seek professional advice tailored to your particular circumstances.

Hilton Bradley Lawyers

Specialist Insolvency & Litigation Firm

Hilton Bradley Lawyers is a specialist Australian legal practice focused on insolvency, restructuring, commercial litigation, and debt recovery.

Learn more about us →