Enforcing a judgment is easy in theory and hard in practice. You can't garnishee a bank account you can't find, or seize goods you don't know exist. An examination notice (and, if that's ignored, an examination order) is how you make a NSW debtor tell you where their money and assets sit before you commit to enforcing the debt. This guide covers how examination works, the difference between a notice and an order, the timeframes that apply, and how the information feeds straight into your next move.

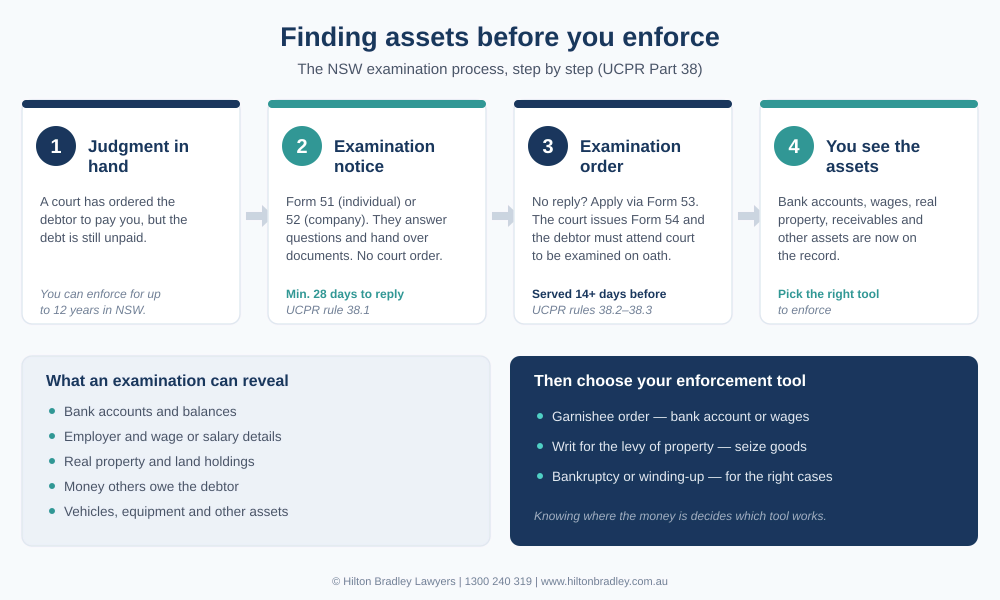

You've won. The court has handed down judgment, the debt is confirmed, and still nothing happens. The debtor won't pay, and you're left guessing where their money is. That's the moment an examination does its real work. Before you commit to a garnishee order or a writ, you need to know what's actually there to chase. In NSW, the examination process is the cheapest, most direct way to find out.

What is an examination notice?

An examination notice is a formal demand for financial information that you, as the judgment creditor, serve directly on the debtor, with no court order required. It's issued under rule 38.1 of the Uniform Civil Procedure Rules 2005 (NSW). You use Form 51 for an individual debtor and Form 52 for a company.

The notice does two things. It requires the debtor to answer a set financial questionnaire covering income, assets, liabilities and expenditure, and to produce supporting documents such as payslips, tax returns and bank statements. The debtor must be given at least 28 days to respond (rule 38.1(2)), and it's sensible to allow a few extra days for postage on top of that.

Because there's no court involvement at this stage, an examination notice is quick and inexpensive. For many debts it's enough on its own. Faced with a formal request and the prospect of court if they ignore it, plenty of debtors simply answer.

Examination notice vs examination order

The notice is the first step, and the order is the escalation. The table below sets out the main differences.

| Examination notice | Examination order | |

|---|---|---|

| Rule / form | UCPR 38.1, Form 51 or 52 | UCPR 38.3, Form 54 (applied for via Form 53) |

| Court order? | No, you issue it yourself | Yes, the court makes it |

| What the debtor does | Completes a questionnaire, produces documents | Attends court to be examined on oath |

| Timeframe | At least 28 days to respond | Served at least 14 days before the hearing |

| If ignored | You can apply for an examination order | The court can issue a warrant for arrest |

You generally can't jump straight to an order for a Local or District Court judgment. The court won't make an examination order unless it's satisfied the debtor was served with a notice and failed to answer it properly (rule 38.3(1)). Supreme Court judgments are the exception, because the prior-notice requirement doesn't apply there (rule 38.2(2)).

Why examination comes before enforcement

Every enforcement tool depends on information you may not have. A garnishee order against a bank account needs the bank and account details. A garnishee against wages needs the employer's name. A writ for the levy of property needs to know what goods or land the debtor owns. Without those facts, you're enforcing blind.

An examination fills the gaps. Once you know where the money is, you can match the right tool to the situation. That might be a garnishee order if there's cash in the bank or steady wages, or a writ for the levy of property if there are assets but little cash. It also tells you when to stop. If the debtor genuinely has nothing, you'll find that out before you spend more chasing it. Examination is one stage in the broader debt recovery process in NSW.

It's worth remembering you have time on your side: a judgment debt can be enforced for up to 12 years in NSW, so a debtor who's broke today may be worth pursuing later.

How the examination process works

- Confirm your judgment and wait. You need a judgment in your favour that remains unpaid. Debtors are generally given time to pay before enforcement starts.

- Serve an examination notice. Use Form 51 (individual) or Form 52 (company), give at least 28 days, and serve it on the debtor. If they answer, you've got what you need, so move to enforcement.

- Apply for an examination order if they don't. Where there's no response, or it's incomplete, file a Notice of Motion (Form 53) supported by an affidavit setting out that the judgment is unpaid, that you served the notice, and that the debtor failed to answer it (rule 38.2). The application can be decided without a hearing and doesn't have to be served on the debtor at this stage.

- The court makes the order. If satisfied, the court issues an examination order (Form 54) setting a date, time and place for the debtor to attend. You must serve it personally, at least 14 days before the hearing (rule 38.3(3)).

- Attend the examination. The hearing is fairly informal, usually before a registrar, and the debtor answers questions under oath about their finances and produces the documents listed in the order. You (or your lawyer) ask the questions.

- Move to enforcement. Armed with the answers, you choose and issue the right enforcement process.

What if the debtor doesn't show up?

An examination order is a court order, and ignoring it carries real consequences. If a debtor who's been properly served fails to attend, the court can issue a warrant for their arrest under section 97 of the Civil Procedure Act 2005 (the relevant rule is 38.6). The warrant authorises the Sheriff to bring the debtor to court to be examined. In practice, that prospect alone is often enough to get a no-show to engage, and sometimes to pay.

One limit is worth noting. A debtor can refuse to produce a document at examination if they could lawfully refuse it on a subpoena, such as privileged material (rule 38.3(5)).

Is an examination worth it?

For a credit manager weighing time and cost, examination usually pays for itself. The notice stage costs little and often produces answers on its own. The order stage involves a filing fee and service costs, but those enforcement costs can generally be added to the judgment debt and recovered from the debtor. Just as importantly, an examination frequently nudges the debtor toward a settlement or payment plan, since many would rather negotiate than sit in a witness box explaining their finances.

There's one situation where it's not worth it, and that's when you already know exactly where the assets are. If you've got the bank details and there's clearly money there, skip straight to a garnishee. And if the debtor is a company you'd rather pressure to pay or wind up, a statutory demand is a separate path worth considering. Examination is for when you're enforcing in the dark.

You can read the rules in full on the NSW Uniform Civil Procedure Rules 2005 (Part 38), and find the current forms and filing options through the NSW Online Registry.

Key takeaways

- An examination notice (UCPR 38.1, Form 51/52) is a financial questionnaire you serve directly on the debtor, with no court order needed.

- The debtor must be given at least 28 days to answer and produce documents.

- If they ignore it, you can apply for an examination order (UCPR 38.3, Form 54) compelling them to attend court and answer on oath.

- For Local and District Court judgments you generally need to serve a notice first; Supreme Court judgments don't require it.

- Failing to attend an examination order can lead to a warrant for the debtor's arrest (s 97 Civil Procedure Act 2005).

- Examination reveals bank accounts, wages, property and receivables, so you can pick the right enforcement tool.

- Enforcement costs are generally recoverable, and judgments can be enforced for up to 12 years in NSW.

Disclaimer: The information in this article is general in nature and should not be relied upon as legal advice. Please seek professional advice tailored to your particular circumstances.

Luke Whiffen

Founding Director

Luke is a founding director of Hilton Bradley with over 20 years' experience in insolvency and commercial litigation.

View profile →